Transcripts

This page contains excerpted transcripts, representing full performances of the piece. As the information presented and questions asked within them represent ongoing research, the collection will grow and change over time.

For ease of navigation, you'll see formatting representing

Transcript Headings

Section Headings

Fun Facts

Spicy Facts

Background/Uncategorized Facts

Audience Questions for Research

as well as hyperlinks to connected conversations, facts, and research.

click a session ID to skip ahead, or scroll to read them all

00A-015 | A004-017 | CBT002-052

Playtest #2 - 00A-015

This Sessions was conducted over zoom on June 4th, 2021. This transcript has been excerpted to remove the large repetitive portions of the Artist talking providing instructions, and edited for clarity.

“Susan: When it comes to my particular lifestyle, you’re either — it’s rare for there to be producers who are like “I’m doing pretty good.” Like, that’s not really how it works. Because either you’ve made a shit load of money or any money you do make you’re reinvesting in your company.

[...]

Jim: Also, side-note, this is a quick digression. Uh, I’m guessing these are three artists you’re talking to, would that be a correct assumption?

Yannick: Yeah/

Susan: Yes/

Sarah: —ish.

Jim: a bit of an odd sample size there. This isn’t like we’re — we’re generally okay-ish with being broke and we’re used to it. Different set of expectations than say, than like, … a real person.”

“Would anything change in your life if [there was no chance of being wealthy, as you define it?]

Sarah: It would change my work ethic. A lot.

Susan: Yeah, I mean honestly if it was like “it doesn’t matter how hard you work, you’re always going to be broke, it’s like “okay cool I’m going to stop doing things that society tells me are better, or the right way to earn money.” and I’m going to be like “Cool I’m going to lean into being broke,” and then do the things I want to do anyway. And stop trying to do them in a way of … where it’s for monetary gain, and more like, because it’s purely indulgent, or because it has impact on the world or wherever.

Jim: Doesn’t matter to me at all. Doesn’t register to me at all. I just—I go in and work my hardest to make the things I want. […] I don’t care. I, I don’t expect to, I honestly expect a struggle, and I find my joy from … process, honestly. And self-discovery. That’s my payment.”

“How likely do you think it is that you will ever be comfortable, by your own definition?

*onscreen, each participant in the group gestures to represent 0-100*

Jim: Pretty good guys!

Yannick: Yeah, that’s quite a page turn from where we were.

Jim: That’s the hope, and it’s the hope that will kill ya. I’m from Cleveland, that’s our motto.”

IF WE WIN 00A-015, September 3rd, 2021

~

click a session ID to skip ahead, or scroll to read them all

00A-015 | A004-017 | CBT002-052 | back to top

~

Playtest #3 - A004-17

This Session was conducted over zoom on June 17th, 2021. This transcript has been excerpted to remove the large repetitive portions of the Artist talking and/or providing instructions, and edited for clarity. For transparency, time stamps have been maintained, where available.

How would you like to introduce yourself?

Vanessa 2:00

Ah, my name is Vanessa. My pronouns are she/her, and I'm currently unemployed.

Heather 2:10

My name is Heather I use they/them pronouns. I like taking strolls in cities.

Juan Felipe 2:18

Hi, I'm Juan Felipe. I use he/him pronouns. And I am on my third pandemic country this year.

[…]

How would you spend $25,000?

Vanessa

It will all go to my student loans.

Yannick Trapman-O’Brien

Yep. And and how would it feel to put 25 down on those loans? What would that mean to you?

Vanessa 17:28

So I owe $45,000 in student loans. So 25,000 will not clear it all out. But it will give me a buffer to be able to then have a more manageable chunk of money to pay off.

[...]

Yannick 17:46

[…] (To Juan Felipe) Can I ask you how you would spend your $25,000?

Juan Felipe 18:08

I have somehow the lamest possible answer. I would stash all of it in my checking account. Because right at a life I somehow have have have not accrued debt. And I usually would have great answers for it. But […] I recently like I recently went from no debt and terrible pay as an academic to really good pay as a biotech person. So I'm making way more money than I've ever even thought I could make. But I don't have a permanent place to live. And I don't know how long we're going to have a job for. So I have a stash that I like —I don’t, I don't know […] buffer. Like, I have no idea what two months from now looks like, down to the country. So even like buying myself like a computer. I'm like, well, that's the thing to put on a plane. And I can't buy plane tickets because I don't know where to. So yeah, that’s, Yeah. 25 in the bank, just in the just in case.

Yannick 19:31

Does that does that feel like a sizable “just in case fund” does that does it feel like most of the cases that would “Justin” are not even— are certainly no Justin Timberlake?

Juan Felipe 19:42

It feels like finding $100 in the street in grad school, it It probably won't solve the biggest problems that I have. But it is more money than I would be able to produce on short notice. So it's good to have but like it doesn't make me feel like it's it It would solve my problems that depending on what the problem is.

Yannick 20:11

[SPICY FACT] A 2018 study found that four in 10 Americans— six in 10* Americans— if they had an unexpected $400 expense would not be able to cover they would have to borrow, put it on a credit card, something like that. And of that population, there's a sizable chunk that just would not be able to pay, period. $400 is enough to just wipe them out.

*[NOTE: I had this right the first time. 4 in 10 would have to go into some kind of debt, whereas “61 percent of adults in 2018 say they would cover it, using cash, savings, or a credit card paid off at the next statement. […] 12% of adults would be unable to pay the expense by any means.” Better, but still not great.]

Fun fact, this piece has never been fun. Fun fact, this year, it feels a lot less fun. Which is the thing that I'm trying to reckon with.

(To Heather) $25,000, how would you spend it?

Heather 20:48

I allotted $5000 for like a rainy day, savings saving situation, a hard $3000 for medical debt, which also wouldn't cover all of it. But it's, that's a sizable chunk that's out of the way that I also just wouldn't have to think about. I allotted $15,000 for like a general redistribution. That feels like a thing that I would want to do if like $25,000 were just dropped in my lap. And let's say I have the $500 for like, spending, but I wouldn't feel guilty about things that I really need to buy for myself. And that's when I stopped doing math.

Yannick

[…] So we've got covering all kinds of expenses. We've got a rainy day fund (indicates Heather), we've got a larger rainy day fund in the middle of a hurricane (indicates Juan Felipe), and we've got I'm already wet (indicates Vanessa), and this would just bail some of the water out of the boat*.

(*If they won**)

** (which they didn't)

How much is $25,000?

??

Not much.

??

Yeah, not that much.

Juan Felipe 23:08

Yeah, when you were saying —I learned to measure currency in grad students. It's one grad student. How much you have to pay a person to be a grad student for a year.

[…]

Yannick

What would it feel like to lose $25,000? Lightning? What was their life ending? Life ending? Yeah,

Vanessa 24:08

I mean, is it you know, 20 to 45,000 in the hole plus an extra 25,000. It's just another number that I will never be able to pay off.

Yannick

Another question for the group: Is there a number of debt beyond which you don't care?

Vanessa

Oh, I currently don't care at 45,000. I keep waiting, provided to know that we're just waiting. I keep waiting for Biden to pay them off.

Yannick

Like to get like — truly at a certain point. It just becomes like inconceivable, or completely bonkers.

Vanessa

Like, like billionaire money, it ceases to be an actual thing.

Yannick 25:29

[…] Where does your money go? Or when the when the money comes in, where does it go?

Vanessa 25:40

Rent bills, a lot of subscription services that I should probably cancel, but you got to watch everything now.

Yannick 25:52

[…] Anyone else?

Heather

I've got something.

Yannick

Where your money goes?

Heather 26:11

Taxes. I do not understand taxes. Yeah. I don't get it.

Yannick 26:19

When you do taxes, do you do them yourself?

Heather 26:23

I do. But like mine aren't that complicated compared to you know, someone like you?

Yannick 26:28

When I do taxes, and I have someone help me now because my taxes— you know, in like 2019, I had 23 employers, so it was just a disaster. That person could tell me any amount of money that I owe, and I would nod my head. “Oh, absolutely.” “You owe $79 billion.” I'd be like, “yeah, yeah, I didn't write receipts. I didn't save enough.”

[…] Speaking of taxes, here's an interesting question. Because we talked about how you'd spend the money. How does America spend its money? Well, we've got Federal spending, for 2020. And for 2019. Which would you rather know more about?

Vanessa

2020

Juan Felipe

Oh, God, I don't want to see—

Heather

(Laughing) I’m terrified!

Yannick

Well, I can tell you that 16.5% just go straight to Social Security. 11.9 to Medicare, seven to Medicaid, small business assistance this year was 8.8 employment 7.3. That already, that's just this half of it gone. That's just half the money all gone. I find one net interest on the federal debt is 5.9%. That's more than twice what we spent on COVID Relief. So America is also paying into a hole that it maybe almost certainly has ceased to care about. And then you've got this military spending this year was 10.5% 2019 (was) 14.7%. So we're, it's not that we're saving money so much as we're just spending so much more money on others. And then you've got the great and glorious other 24%.

Yannick 28:48

Remember that you can ask your question at any time. Or if the just constant bludgeoning of bad news becomes too heavy, you can slap in, and hope that there's a fun fact in here. There might be, the only way to find out would be to slap the table approximately 20 times.

Juan Felipe

I've played that game with Twitter every day when I wake up and make the mistake of checking my phone.

At what annual income does wealthy start?

Yannick 30:49

Okay, I got “$120,000” (Juan) I have “a million passive” (Vanessa) . And I have a million (Heather). What's passive income, Vanessa?

Vanessa

It's when your money makes money for you.

Yannick

It's when your money makes money. It's just sitting in a an account and you are living off its interest. It is the interest on Yes. Which the grand joke is —or the the sort of disparaging comment that often gets made is, “the lottery is gambling for poor people; Stocks are gambling for wealthy people. But the odds are a whole lot better.”

Heather

Where does multi level marketing fall in that equation?

Yannick

I think multi-level marketing is gambling for people you went to high school with.

(Laughs)

Juan Felipe 31:56

I was gonna say it's gambling, but you're buying it from a dude, that's totally good for it. "There's DEFINITELY a winning ticket."

(Laughs)

Yannick 32:06

Hey, okay. Um, question for the group, you're going to type your answer in the chat and we're going to do it on three. At what lump sum does comfortable start this amount of money is wired to you no strings attached tomorrow. And with that amount of money, you have become comfortable magic that day, that like it'll, you know, assume that it hits and you can spend it that day. In 3,2,1! (Juan Felipe $2,00,000 - Vanessa $25,000,000)

Interesting.

Okay. So for now, everyone's —pending an answer from Heather—

Heather

I feel like I undershot it is the problem! (all laugh) I'm looking at everyone else's. This was mine ($50,000).

Yannick

Yes. So just to be clear, um, Vanessa and — Vanessa, your amount to be comfortable? Is —

Vanessa 33:16

— I grew up very poor. There will never be an amount high enough to leave me comfortable.

Yannick:

So you would feel wealthy before you feel comfortable?

Vanessa:

Yes.

Yannick:

Uh, question from a stupid person: ‘what is the fucking point then?’

Juan:

… to not get eaten by capitalism.

Yannick:

It seems like the point is to eat capitalism before it can eat you.

Juan:

No, $25 mil does not make you eat capitalism. you are a baby to capitalism at $25 mil. But you might be comfortable.

You can live another like—

Yannick 34:01

—but your your answer is —and math is not my strong suit here— but I'm going to say you could- (exhale) you could- you would- with $2 million, that is the same as being wealthy annually for six years (based on his earlier estimation). Plus.

Juan Felipe

Yes. I like, with uh, I think I'll uh— like Vanessa is really capturing the spirit of, if you grow up in like a low-trust scarcity environment, uh yeah, you holy shit the level of guarantees you would need to give me for the number to really like make sense, is nuts. With 2 million I'm like, it's comfortable in that with when when I think about going to bed that night. And that night not being like "fuck fuck fuck" like trying to do the math. I think like around 2 million I think I start being like "tomorrow is gonna be okay," like "There's a problem long term, but like tomorrow, I'm gonna like tomorrow's fine, tomorrow's fine." Like if I lose a million tomorrow, I have a million dollars. So. (exhales) But yeah, I think comfort is a very tough word to ... use now.

Yannick 35:17

I want to ask about that. Because I wonder, do you all feel that these numbers are higher across the board than they would have been before 2020?

Vanessa 35:29

No, I think these numbers started getting ridiculous, you know, probably around—I don't know, when we started letting billionaires be a normal thing to us.

[…]

Yannick

[…] I wonder how much it feels like one purchase has the power to really shift these numbers around. Because the second that you're trying to think of purchasing a place, or like buying a house; Or the second thing you're trying to think of, like the amount of money it takes to relocate your life; I wonder how much that changes those numbers? And I wonder if they ever change back?

Juan Felipe 41:53

Well fingers crossed that they changed back. Yeah, I think that throw away a very throwaway comment, I was gonna make it. I know if it's my personal reaction. I like propensity to this, but with a lot of these questions. It's almost like a trick. Like, like, it's really easy. When it comes down to money to feel like I'm like signing a contract. And I've been very used to almost being like, like, cheated by not being like an asshole and asking for tons of money for everything. And so, you know, if I hear like, how much money would take in one lump sum to be comfortable. To me, at this point, I'm just like, Okay, what is the number that I'm not going to regret answering to this? If there's, if like, something happens, in terms of the whole measurement, especially comparing to like, l the guy who own the lottery— I'm just kinda like, "yeah, and like, What does his brother do? And what is his dad do? And what does his mom do? And what do the grandparents do?" Cuz? Sure, I believe that this guy makes $140,000. But there's a dynastic aspect to a lot of the high incomes in the United States. So right now, I know that I'm making like, I mean, like to like, even like, break it.

This is uncomfortable, because we're socialized against it. But like, I was making 30k a year for years, two years ago, and like, this year, I'm supposed to make $150,000 like, Holy fuck. Like, I don't, I can't, because that's, that's five of me. That's five of us. I rent my apartments. Yeah, yeah, it's like so many grad students. But with this whole, like, emergency, like, I don't have a like a family network or anything like in this case of emergency, I'm like, at no amount confident that I'm not going to be in the red. Because there's not like the family house that I arrive at at a place or like, oh, like, "my father, just like took care of _____" or even just like "my father has some connection somewhere. So this was something that I didn't need to invest time and money into figuring out." Yeah, like, there's even just like the friend—the friend network that you have in a given place, and their wealth is part of how realistically you should calculate what your wealth is. So as an answer to a lot of discussions I'm like "me by myself, with the support, I want to be able to give the people that I love? And the support that they can offer me their income levels? Like, yeah, like $200,000 a year is when I would start thinking that I can like, not just, like, survive, but also be able to, like, do what wealthy people do, which is to help their loved ones.

(Editor's Note: This idea of wealth as being defined by needs larger than an individual comes up in CBT002-052)

Yannick 44:53

Yeah.

Heather 44:56

I think besides not being able to conceptualize like, what You know, even $500,000 a year looks like. Like, I think one of the reasons I tend to undershoot it a lot is like, I still don't know how to ask for more money. Like, I don't know how negotiating my salary works, because I haven't had to do that yet. Um, and, you know, we're told to not ask for more money, like, that's not, you know. And I think another reason that my, like, yearly comfortable is is so low is because I don't I can't let it set in that there are so many things that I'm not able to do right now. And, like, in the context of my life now, and the things that I want to do, like, I'm fine, and like, I'm healthy, and I feel okay. And that's all I can ask for right now. And, I guess, like, in, I think if I were fully in the spirit of imagine, you know, the largest stack of bills you can for yourself, like, yeah, my number would definitely be higher. But I guess I just, I don't know. I, I can't get there right now.

Vanessa 46:13

Yeah, I mean, I mean, I, you know, I will shoot for the moon because I know I'm not getting in a rocket tomorrow. Yannick doesn't have to have access to these monies for me. So like, my number could be as friggin high as I could possibly think it, because it's not going to happen. I-you know?

Heather

Yeah.

Vanessa

And it’s-I don't know, I'm currently you know, looking at buying an apartment. So I'm currently always looking at my finances now. So I know how much Ian and I need to be like, great. "We are looking for an apartment. This is how much we need for a downpayment. This is how much we need for closing costs." You know, I'm looking at these hard numbers. So my, you know, what I need is more, like tangible for me right now.

Yannick 47:05

Well, here's something I'm gonna throw out because I — there's something that Juan Felipe said that really resonated me with this idea that like, that, the amount— you know, your your, your income can change— I'll say that like, for me when I got to $25,000, it was a moment. But that felt that felt as big as a jump because I was at 10 [Editor:10k a year] for a while, right? And doing this piece in Philadelphia with a bunch of theater people, I hear numbers like that a lot. I mostly hear like, "Oh, 10,000, I made 8000 last year, right." And so it was this way that I feel like the quantum leap. And I feel that sense that I'm like, there was not even a moment of relief. There was not a second in which I was like, "it's enough." And so I think one of the questions that I keep coming back to over and over with this piece is this idea of like, just what-how much power do members have as they get bigger? And like how does, how does the way we relate to them change?

[…]

Yannick

So I have one final rapid round and then we're going to scratch this goddamn ticket here's my question type of the face to bottom the face using your own amounts that you said do you believe by your own definition that you will ever be wealthy?

(Group estimates and places hand between top and bottom of head)

Yannick 53:26

I've got I've got uh, a chin, and two real cute shoulder cuts.

(Laughs)

By your own definition, do you believe you will ever be comfortable?

Vanessa 53:43

it's so it's a waver-y—I know I can make myself comfortable with my salary.

Yannick 53:51

but that's that's comfortable coming down to meet you, not you going to comfortable where you said (it was)—

Vanessa 53:56

That's me redefining my comfortable

Heather 54:00

I think that's my relationship with "wealthy." I just can't think about anything higher.

Juan Felipe 54:10

I just thought we're going by like —our, our monthly comfortable numbers. I think pretty high. I picked them, like a not insanely high one out of sheer guilt of thinking that, I could ever deserve that amount the money. Uh, Christ.

[…]

[The group (finally) scratches their lottery ticket]

Juan Felipe 1:02:51

This has a lot of YouTube potential for some reason.

Yannick

I did this piece in part, because I want to understand why would I unscratched that $100,000 A part of me got excited why? it's so stupid. I can sit here and tell you I know the exact percentages, the chances that you would win that ticket, I have bar graphs— I went and I took their numbers from their official rule sheet. And I ran them through and I double check them against each other to make sure that they're actually being fucking honest. I know their odds, I know it cannot happen. But as soon as I see that $100,000 A part of me still believes "they're gonna win at all." Which I always do, and I'm gonna scratch your bonus.

Juan Felipe

These things are so fancy.

[...]

(Yannick scratches the final prize slot)

Yannick 1:03:44

And because the word "mother" does not appear, it means that you have not won. So this is now a losing lottery ticket. Which is where this piece kind of started for me. It ended with me going at 4am from gas station to gas station in Philadelphia, asking the attendants "Hey, do you have that best mother ever lottery ticket"— weeks after Mother's Day? Only to finally have a man say to me? "Yeah, but we have a policy; we don't sell a lot of tickets between 8pm and 9am. It is not an hour for you to be doing this thing that you were doing." Because when he said "yes," I immediately said "I'll take 10" (group laughs). And I pray that that that man called his mother that night. This piece started for me is that—and Heather knows this —in 2017, I think this was the year that I started noticing because I was working in Center City in Philadelphia, and as I would walk around, I would just find spent lotto tickets all the time. And I swear to you, I'm sorry to curse this to you— Vanessa you'd like going around and seeing shit on the street, so I think you might be into this— You will see them all the time, if you look for them. And at a certain point I just kind of got obsessed with, like, I thought it was the weirdest thing to be finding. And at a certain point I started to feel uncomfortable, because I started to feel like this was an incredibly intimate thing to find, like such a weird sliver of somebody's ... hopes, expressed. And at 26— 25? no one knows —at the time, and feeling very "young, dumb and Marxist," A part of me was like, "well, that's America, in one image." Which is it's a lottery for a million dollars, and someone's gonna win it and it isn't you. But you might. What happens with this ticket now, is that I get to answer part of that question, which is I wanted to know, what were people going to spend their money on? So this is going in the Book. (shares book of past participants). You can go and see what all that meant. This is a really weird book. Because all of these entries you're seeing are from 2019. And none of those people know what's coming.

Juan Felipe

Hm

Yannick 1:06:16

Every time I see — like I've been transcribing, I have to tell you guys— every time I see savings, there's a part of me that's like, "Oh, thank God," and a part of me, that's like, "it's not enough." Like, "they didn't win, no one won more than $10. Why does it matter to you?”

(Laughs)

But, there is something to—you know, Juan was the one who brought up the idea of the taboo. That like, "whatever you do, don't say how much you make." And I brought up the taboo of, "whatever you do, don't go to New York and tell people how much your rent is in Philadelphia." Right? And I honestly, I care a lot about care. And I understand that, in some ways is a function of care. But I wonder who we're actually taking care of when we do that? Which sounds like a neat resolution to this piece. But there isn't one because I don't know how this piece ends yet. I think I'm still trying to find out what this piece is about. Because I think at the end of the day, I still find that lottery ticket. And as soon as my mind tries to comprehend an amount of money larger than $10— which is still what Yannick believes a sandwich should cost no more than, in the year 2021 of our Lord— as soon as I try and think about a number bigger than that, it all just goes kind of fuzzy. So maybe this is me trying to start by understanding any number bigger than that. I thought I'd start at $25,000.

[…]

Yannick 1:09:27

My last question for each of you. Was this a fair trade? Vanessa starting with you.

Vanessa 1:09:38

Was this a fair trade my time for this art experience?

Yannick 1:09:43

Yes.

Vanessa

Yes

Yannick

Juan Felipe, was this fair trade?

Juan Felipe 1:09:52

Oh, absolutely. I think I get more out of that you that so maybe not. But to my benefit.

Yannick 1:10:01

I think we agree as a group, that we're comfortable with that.

Juan

(Laughs) right.

Yannick

Heather. Is this a fair trade?

Heather 1:10:13

Yeah. I definitely think you put a lot more work. So do you think it's a fair trade?

Yannick 1:10:20

Well, here's the funny thing. The only reason this piece is legal, is because — I had to call around to find out whether or not this constitutes a game of chance, I am giving you a lottery ticket in exchange for something, which means by my own definition, I'm selling it to you. I had to call about six different city and state agencies, all of whom directed me to each other, and would not believe me about that until I started referring to the representatives by name saying; "You are about to connect me to Mike, are you not?"

(Laughs)

I got someone from the PA gaming board. I explained the project to them. And they said, "well, it's fine. Look at this section of the law, it says you're allowed to give away lottery tickets as gifts." I said, "but it's not a gift. I'm giving it to people in exchange for their time and their opinions." And he said, "Yeah, but those things don't have value."

(Laughs)

So thank you all for sharing something of debatable value with me today. I have no idea what I hope this accomplished. So I hope we accomplished it.

IFW A004-017, June 17th, 2021

~

click a session ID to skip ahead, or scroll to read them all

00A-015 | A004-017 | CBT002-052 | back to top

~

HOW WOULD YOU LIKE TO INTRODUCE YOURSELF?

Lauren 3:13

I'm Lauren or Lj, I use both names, because there are lots of other Lauren's in the world. So inevitably, I default to Lj. I'm LJ.

Yannick Trapman-O'Brien 3:23

Cool.

Mae 3:25

I'm Mae. I use they/them pronouns, and I think that was a very smart decision to return that razor (Note: Mae is referring to a brief story I told about returning a razor after using it because I needed the money for bus fare).

Lilly 3:35

I'm Lilly, uh- yeah.

HOW WOULD YOU SPEND $25,000?

[…]

Lauren 13:09

Well fuck, I want to ask you questions about what I could do with the money. Put down assumptions first?

Yannick 13:18

I mean, feel free to ask us a question. You just have five minutes. So what's the most important question?

Lauren 13:22

So like my first thought is like, I want to give it to somebody who like knows what the fuck they're doing. Like I have an aunt who like is very good at making money get bigger. So and now realistically, I can't give her my $5,000 but I could give her my 25.

Yannick 13:35

Consider you have won $25,000 in this hypothetical situation and it's yours to control so you can do with it whatever you want. And if your answer is I would give all of it to my aunt who's good with money. That works. Right? But you have to demarcate

Lauren 13:47

But I think my question is, like, how much does it typically cost to have like a money manager like that? Because I feel like-

Yannick 13:55

An excellent question. How much does a money manager cost? I will add that to the pile. I don't have an answer for you yet.

[EDITOR'S NOTE: we chased this down. You can find the full answer and more resources/links at the questions page, but to summarize: 0.5% to 2% per annum, depending on the portfolio size, or anywhere between $75-$150 for daily money management.]

[…]

Lilly 14:17

I'm gonna run for water real quick.

Yannick 14:19

Run for water, you got some time.

Lilly 14:22

Water is ran.

Mae 14:25

Wow, that was quick.

Lilly 14:26

It was on the ground. Didn't know you guys were sitting with Usain Bolt, did you?

[…]

Lauren 17:26

Wait, can I smack with questions?

Yannick 17:28

Yeah, go for it

Lauren 17:29

So like, say I get my $100,000 prize from Lotteria Don Clemente? Do they- do the vendors have to toss out all of the other tickets that are like this once all the prizes are gone?

Yannick 17:42

Oh, no they absolutely do not. Pennsylvania lottery simply reports if you go on their website and check how many prizes remain, right. However, the Pennsylvania lottery does eventually close sales. I've asked vendors, what happens when a sale closes. They have all told me talk to my manager. So I'm still working on that one. They closed sales, however, a year — up to a year after sales are formally closed, you can still claim the price.

Mae 18:16

Do one more

Yannick 18:17

Yep. Do one more. One more.

Mae 18:18

Okay, one more. How much we have to pay in taxes?

Yannick 18:22

Oh, I love it. Okay, this is- we're quick now. We are only- gosh we're only 12 minutes, in normally we get to about 40 before someone realizes there are three of you and it's $100,000 ticket, how much do each of you get?

Mae 18:36

Taxed?

Yannick 18:37

So the federal government will automatically take 25% of lottery winnings for a prize over 5000.

Mae 18:45

Of course, of course. So 75,000

Yannick 18:48

Since January 1 of 2016. The state of Pennsylvania taxes lottery winnings at income tax rate of 3.07%. When you get past $600, they will automatically send you a W2- a W2G which will report your lottery winnings. When you get past $5,000 they will automatically withhold, from your winnings, the income tax and will also send that to you. I have talked to the Gaming Commission, recently, because someone asked then do you get taxed again? The answer is no. It's taxed- it's a separate category of taxable income, and they just take it right up front. So you would all have to reckon as residents of the great state of Pennsylvania, I assume but don't know for sure. You would have to reckon with your state income tax. But the federal government takes 24% Bing, bang, boom right off the top. So your actual amount, you'd all come to about 26,000 you'd lose a good chunk due to taxes. If you want to get into the weeds about taxes, that's fun fact territory we can slide later.

Lauren 19:48

Kind of wild is a reflection that so few people get winnings of that like amount but yet we have a very clear process on how to pay tax on it.

Mae 20:01

The government takes ya money.

[...]

HOW WOULD YOU SPEND $25,000?

Lilly 20:57

[…] I said I’d give the $25,000 to my parents.

Yannick 21:08

How would it feel for you to be able to do that?

Lilly 21:13

I'd cry.

Lauren (whispered)

This got serious very quickly.

Yannick 21:19

Yeah. How do you think they would feel? If you did that?

Lilly 21:24

I think they would also be very appreciative.

I don't think it make it any easier on them.

Yannick 21:31

Yeah.

Lilly 21:34

But it's something?

Yannick 21:38

Thank you for that.

[…] (to Mae) How would you spend your 25,000?

Mae 21:45

This list that I have, and God, I could probably make a million different versions, what came out was 15k invested in a community space. 5000 for immediate pleasure. And 5000 for immediate mutual aid.

Yannick 22:03

I have to say that the term “immediate” is really doing it for me in that, because I get people who talk about pleasure spending or fun spending or things like that. But immediate is such a gratifying modifier. I'm curious, what when you say immediate pleasure, do you mean that that $5,000 would be spent tomorrow?

Mae 22:29

I'm not necessarily, more so that I would just allow myself to- I take a long time to make monetary decisions. And so just allowing myself to not overthink it. And if I go out one day, and I'm like, I want to get food today, or I want to get someone else food or whatever. I'm allowed to do that without sitting there and stressing about it.

Yannick 22:58

It's $5,000 of unconsidered spending. […] $5,000 of not calculating your spending. $5,000 of just being like, “I want that, I get it.”

Mae 23:08

Yeah, exactly.

Yannick 23:12

Have you ever had a pot of money like that?

Mae 23:17

Kind of? Yeah, yeah. Yeah. I have up and down. To me- I don't know. I don't feel like I've ever- I don't allow myself over, like $1,000 to even consider making a decision about that much money without it being real decision.

Yannick 23:41

Yeah.

[…]

Lauren 23:46

When you first started talking about this, I was like, I was like, Do I have a pot of money? Or am I just irresponsible? Cause I feel like I spend money like that. But then you just said anything that you're purchasing that's above $1,000. I was like, Damn, I haven't bought anything worth more than $1,000

Mae 24:03

That's true. That's I mean, above 1000-

Lauren 24:06

Other than a car

Mae 24:06

But that's the thing. I'm taking that as like rent.

Yannick 24:10

Sure

Lauren 24:10

Okay, got it

Mae 24:10

Anything that's like less than rent, but in reality everyday, I guess. Honestly, every purchase I make is like highly

Yannick 24:18

Considered.

Mae 24:18

Considered. Unless it is for other people or someone in need.

Yannick 24:29

Which is where the idea of immediate comes in to the ability to sort of skip that process. Thank you for that. Yeah.

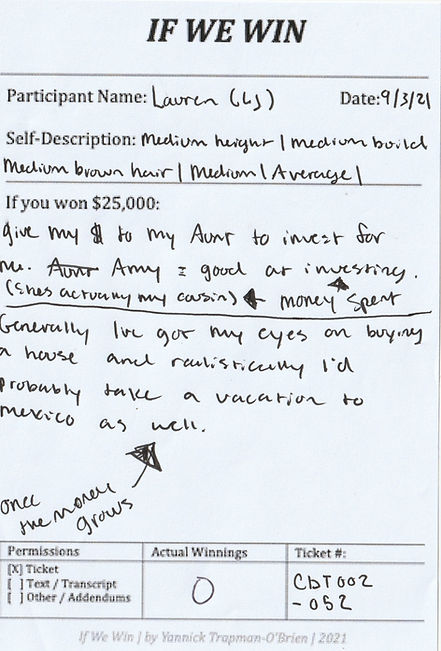

Lauren 24:37

All right, y'all. I kept calling her Aunt Amy, she's actually my cousin. Sorry, Amy, just in case she comes to see this and sees this. I made sure I corrected that.

Yannick 24:49

Cousin Amy's gonna charge extra for that.

Lauren 24:52

I got a cousin Amy and she's good with money. Um, she's a investor. I don't know what that means. She might just be in the mafia. But I've seen her turn money into bigger money. So realistically, most of that's gonna go in there. What am I going to do with that money that she builds out? I took a step further because I felt like that was a very generic answer, followed up by two more generic answers, which are,wanna buy a house. I'm like saving on my pennies right now. If I had that 25, I'd be like, Oh, fuck, yeah. Okay, great. Now I'm doing it without question. I wouldn't be like, Can I actually afford this? And then realistically, I'm probably gonna take a vacation as well, if I have money sitting in my bank account, because I'm not a thoughtful spender. I'm an immediate spender.

Yannick 25:39

Okay, so. So for accounting purposes, I have to ask you, the full $25,000 would be given, lump sum, to cousin Amy, the idea of wave your money wand on this and make it grow?

Lauren 25:51

Yeah

Yannick 25:51

You're not holding any [back]?

Lauren 25:52

I don't think so

Yannick 25:53

That's not me questioning. It's literally just for accounting purposes, I will. So I take all these answers, actually digitize them, and I run the numbers. And so I can report out percentages, I'm happy to tell you why that's functionally meaningless, because you are not what we call a representative sample. The purpose of this research is not to produce a chart that says this is how people spend their money, the progress of normal data is that data is taken from you it is aggregated and it is presented as representing some larger hole. Basically, this is the opposite. I am sitting on a bunch of the larger data, which I am making it my project to present to you, so that you can aggregate it to understand your- they call it n equals one, sometimes, which is sample size of one. This is findings that are relevant just to you. They're not general rules. You're not here to answer the universal question. You're here to answer your questions. Or, in this case, I'm here to your questions. You're just sitting across the table from a man in sauna.

Cannonball Tests - CBT002-052

This Session was conducted with an in-person audience in rehearsal for the Cannonball Festival, September 3rd, 2021. This transcript has been excerpted to remove the large repetitive portions of the Artist talking and/or providing instructions, and edited for clarity. For transparency, time stamps have been maintained, where available.

HOW MUCH IS $25,000

[…]

Lauren 27:09

Not that much money.

Yannick 27:10

Not that much money.

Mae 27:11

So much money!

Yannick 27:13

So much money, not that much money, so much money.

Mae 27:16

And also not that much money at the same time.

Yannick 27:20

You- something that we kind of talked about is is this idea of like, I can't now but in the future, like you said, you would want to grow the money so that you can take a vacation, buy a house. How much money is enough money that those things start to feel like I will consider ______?

Lauren 27:38

Achievable. Already considered- already considering the house and the vacation? So I feel like that, but I feel like that's more about like cushion. Like, technically, cousin Amy doesn't start accounts until you make like $50,000, but I feel like I can be like, get in there and be like, come on Amy, help me out. So- or I think even more than that. So like, which is my question of like, how much does it actually cost to have a financial advisor and like nobody, like people aren't going to take my 25 case seriously, even though it's huge for us. It's not huge. And in the grander scheme of things,

Yannick 28:12

I'll say two things. One, is I don't know. One is I don't know. And I'm gonna find out. Two, is now and throughout this piece. I want to encourage you not to consider the man sitting at 80% in a sauna, as a form of like legitimate financial advisment, but will present facts which we will use to make decisions. The third thing I'll say, is that often, the way that people who are managing money if it is in an account that is being invested, get paid, is they get a portion of your dividends. […] Which, in general, if we have questions about investment, and that's the thing that you're curious about. What I'm going to tell you is that this piece is about to open out to a degree, […] [but] before we do any of those things. I'm going to hold up my end of the bargain and we're gonna play the lottery.

Lauren 29:42

Oh fuck

Mae 29:42

Alright

[…]

Lauren 29:52

Wait, are you gonna scratch the card?

Yannick 29:54

Oh no. It's your card. […] You have to scratch it.

Lauren 30:00

Oh, I want Lilly to scratch it.

[…]

Lilly 30:59

I'm shaking.

Yannick 31:04

[…] I do wanna ask the group, we're gonna be doing something called top to the bottom of the face. Top to the bottom part of the face, How likely do you feel it is that you are about to win? $100,000. Bottom is zero. This is like, I'm not saying the actual odds. I'm saying what do you feel right now? […]

Lauren 31:32

Emotionally, I feel like I'm excited to invest this 25k but I don't- I don't- I don't know. I feel like you have some sort of intuition when something like that's about to happen.

Lilly 31:42

You know what? Scratching is very therapeutic. Which is a bad thing for something addictive.

Yannick 31:51

Interesting you say that, how about a free spicy fact?

Mae 31:55

Yeah

Yannick 31:56

Because you just said addictive which makes me think of a book that I very much enjoyed. […] So let's talk about some findings from the Power of Habit a book by Charles Duhigg. Published in 2012. We talked about addictive. Well, a 2010 study from cognitive scientist, Reza Habib, always trying to make sure I say the name, found that the brains of pathological gamblers responded in the same or similar way to a near miss on a slot machine as to a win. So they were scanning their brains and when it almost went off, their brain fired the same way or similar to as when they won. Worth noting, this was just a video of a slot machine. And they were told you won't be winning anything, but just watching it is enough to make anyone's brain be like "ooo". For non pathological gamblers, watching a near miss, they responded the same way they did with a loss, which was cool. For a pathological Gambler, the same mechanics fire away. We know that slot machine designers know this, because in the late 1990s, they hired a former video game executive to help them design new slots. And the biggest innovation of that was to increase the number of near wins. The non state lottery executive was quoted in 2012 saying every other scratch off ticket is designed to make you feel like you almost won.

Lauren 33:34

(sound of agony)

Yannick 33:35

He described it as like pouring rocket fuel on a fire.

Lauren 33:39

Um, I feel that. I feel like I have had many close close lottery tickets.

Yannick 33:44

You have not.

Lauren 33:48

What- what percentage of people are pathological gamblers?

Yannick 33:51

What an excellent question; (writing in notebook) “what percentage of people are pathological gamblers?”

[…]

Mae 34:05

Can I ask another question? […] The question that I'm adding to this is, "is it genetic?"

Yannick 34:18

"Is it genetic?" Great question.

Mae 34:21

Or is it just socialized?

Yannick 34:24

Great question

Lilly 34:25

It can also be associated with certain mental illnesses, right? Like you're more likely to do something if you have one.

Lauren 34:30

Like people who are manic tend to go crazy gambling.

Yannick 34:33

I cannot confirm these things because they are not in my stack.

[…]

Yannick

Let me give each of you the chance to choose ‘Spicy’ or ‘Fun’ fact. (to Lauren) You requested “get good at money, right?” (Lauren nods) Let's talk about investing. Let's talk about cousin Amy and what she can do for you. Has a purpose after all. Who's familiar with the concept of compound interest?

Lauren 40:26

No.

Mae 40:26

Mhmn.

Yannick 40:27

Good, this just- this I think is a helpful one to understand, because it's a lot about how money works. And actually, once you understand this, you understand how most of our systems work. 'Compound Interest' means that when you have $100 in your bank account, and you get 2% interest, at the end of the year you have $102. And the next year, you don't get another $2, you get 2% of $102. Your gains compound over time. However, this depends on your interest rate. So we're going to use compound interest to understand our first get "get good at money" thing, which is your A. P. Y. Your annual percentage yield, for your bank account—if you are banked, which many people are not. If you are banked. Your account has an APY. The average at big banks is a staggering, big dick energy, .01 percent.

(laughs)

Yannick 41:24

That is what my bank gives me every bleeding terrible day of my life. The national average, on accounts, is .06%. Still not great, interest rates are pretty low right now. A high yield savings account, which many of them are available online, could offer you as much as .6%. How much does this matter? Well, let's say that, uh, we are one of the pathological gamblers we know out there, and we play the lottery once a month, every month. Let's say instead of doing that, we take our $5, including this $5 (indicating ticket) we put in a bank account every month. And let's say we do that for 60 years, if that bank account offered us no interest, we would have $3,600

Lauren 42:07

And no fees.

Yannick 42:09

If that bank account had no fees! Realistically, they probably hit with the fees.

Lauren 42:13

I lost 50 bucks past five months, because I have a separate save— like I have my my account that I use often, and my like bank account that I just put my savings in and I lost 50 bucks because you have to make like a transaction every single month, or they charge you 10 bucks. But I do make .01% interest this year.

Yannick 42:32

So if you're putting that money in and you have point .01%, at the end of 60 years, you'd have $3,615. Not that impressive. A point .2% increase but not that impressive. Let's say you would .06% interest; you'd have $4,325. Getting somewhere. Let's say you had the kind of return that a high yield savings account used to get you, and what you can still in some places: find 2%. You'd have $6,859 at the end of that time. Let's double that. Let's say you've got a really competitive interest rate that you're getting— maybe you're doing bonds or things like that, which I promise we'll talk about if you want /

Lauren 43:08

/Thank you

Yannick 43:09

/You would have $14,332. Let's say, you were have the same interest rate or rate of return that the S&P 500 has averaged over the past seventy years: 7%. Which a lot of people take as sort of like a rough estimate of what you can expect to make on the stock market if you play long. You'd have $49,100.96. A net gain of 12,062%. Compound interest is bonkers. (laughs) You, getting point .01% in your bank account, not only are you not getting that (7%), but you are not matching inflation. Which means every day your money actually is worth less than it was the day before.

Lauren 43:10

Uhahhhhhhhhh!

Yannick 43:29

Feel good facts! Pew pew pew!

Lauren 43:59

What this just confirmed for me is that I'm very happy to give my money to somebody else, because the first sentence he said, I was not listening at all (laughs).

Yannick 44:08

I hear you. I appreciate that. I'm going to attempt to summarize it in a way that can that can get you.

Lauren 44:13

I think it's a my inability to listen to numbers. I think to remember four numbers me and mae had to sing it like five times.

Yannick 44:21

Challenge accepted. Challenge accepted, with my remaining time, however long it is. Think of it this way, which is- your money, you want to give to your cousin Amy to hold, but right now you're giving it to the bank to hold and they get to use it.

Lauren 44:35

Bitches

Yannick 44:36

They're paying you for that loan. Right now, they are paying you less than your money is valued. And and and our success rate so we are essentially trying to catch wealth and it's doing that. High yield savings account is increasing the amount the bank pays you to have your money

[…]

Yannick 55:13

Things you can do with your money. Which brings us back to this notion of what is money? Like, what does it represent? Value wise? $25,000 is not a lot. It's lot of money. It's not a lot, they shaking their head, right? But when I asked how much is $25,000? You guessed it.

Lilly 55:33

It's just enough to do nothing.

Mae 55:36

It's just enough to do nothing

Yannick 55:37

It's just enough to do nothing

Mae 55:39

Write that down! That's good.

Lauren 55:42

Yeah, I'm looking at this. I'm like, even $100,000. Like, my tuition was 45 a year.

Yannick 55:48

Well, what a fantastic transition to our lightning round.

Mae 55:56

WHOOOOOOO

Lauren 55:59

Perfect.

Yannick 55:59

Okay. So, in this round, we're going to explore these thresholds of money. [...]

At what lump sum [...] would you be wealthy?

Yannick

This isn't- you're not searching for the right answer . It is your answer. What lump sum would you be wealthy? An unfortunate thing is I'm going to make you answer in seven seconds. Your all gonna answer at the same time. Seven, six -

Lauren 56:26

A million

Yannick 56:26

five, four, three, two, one

Lilly 56:31

2.5?

Mae 56:32

500,000

Yannick 56:33

2.5 million. 500,000. Okay, great. Keeping the lightning round going, at what annual income would you become wealthy?

Mae 56:45

Dammit, I misunderstood the question.

Yannick 56:47

Was 500,000 your annual income answer?

Mae 56:48

Yes.

Yannick 56:49

Okay. What is your answer for lump sum? Hits you tomorrow and you are wealthy?

Mae 56:55

I'd say, yeah, 2 million.

Yannick 56:57

2 million, 2.5 million and a million. Okay. So annual income? I know yours is 500,000? Everyone else has been thinking while I've been talking, the speaking has really functioned in no way as communication. It's just a way of filling the time you have five, four, three, two, one —

Lauren 57:10

I'm gonna stick with Mae's 500,000

Yannick 57:12

500. 500. 500,000. Okay, 500s across the board. What a remarkable demonstration of why I make you all answer at the same time. […]

Lauren 57:42

That's good. I was gonna say six figures. I mean, which 500K is six figures, but more specific.

Yannick 58:15

So $100,000 annual income to you as well. That's not a challenge.

Lauren 58:20

I think if I if I broke 100,000 a year, I would be comfortable. Yeah.

Yannick 58:25

Oh, we just said a magic word.

Lauren 58:29

Comfortable!

Mae 58:29

Ooo comfortable.

Lilly 58:29

Comfortable

Yannick 58:29

Comfortable. Because I think we all know that in America comfortable either means comfortable, means able to make unconsidered spending means buffer. Or comfortable means someone asking you how much you make, and you go well- we're comfortable.

Yannick 58:45

For our purposes, let's say comfortable is the former— comfortable is actually, legitimately, me saying to you, when would you be comfortable? And it's me saying "a lump sum is going to arrive in your account tomorrow." That lump sum arriving, That amount: you feel comfortable now. What is that amount? You have five, four, three, two —

Lauren 59:06

$50,000?

Yannick 59:08

I know that when I say numbers, your brain turns off. I see you watching. I just gotta say - $50,000.

Mae 59:17

20k

Yannick 59:18

20k, 50..

Lilly 59:21

I have to think family wise too. I'd say a million.

Yannick 59:24

A million, yeah. So this is something that came up in A004-17. Someone told me, it came up later well. A participant said they could never be wealthy until everyone in their family was wealthy. Because they are one sick uncle away from not having money.

[…]

At what annual income would you consider yourself comfortable? When do you feel that?

Lauren 1:00:49

[A million]. My numbers don't add up. (laughs)

Yannick 1:00:52

That is the math! And that is the point of this piece. is that, 'money' does not follow math. Money does not follow a linear plot. I think it's a little bit like the difference between quantum physics and Newtonian physics. That like really tiny objects actually don't behave the same way. And why do they behave differently? Large amounts of money don't behave the same way as small amounts. Our brain's constantly shifting gears on how we understand that an amount of money. And 'wealth' is not the taxed the same in this country as income.

(mmmmmm)

Lauren 1:01:28

SPICY FACTS!

Yannick 1:01:29

You can feel the spicy fact coming. Before we do it, I want to hear everyone else's number.

Mae 1:01:34

20k

Yannick 1:01:35

20k

Lauren 1:01:37

Wait, annual salary 20k?

Mae 1:01:39

I mean, sorry. 30k.

Yannick 1:01:40

30k.

Lauren 1:01:42

Is comfortable?

Mae 1:01:42

I mean-

Lauren 1:01:44

Mae, I want to know how much you make a year.

Mae 1:01:47

Depends. Sometimes more than that. A lot of times less. I mean, I think that's the thing for me. I'm like, comfortable. I'm like, do I have housing and food?

Yannick 1:01:56

That's when your comfort level starts.

Mae 1:01:58

I've been a lot less comfortable than that. So for me, I'm like, that's comfortable.

Lauren 1:02:03

Yeah, I guess I've just been so shocked. Like, there was like one point where like, one day all of a sudden had $30,000 in medical bills. And I'm like, all of a sudden, like, yeah, 30k is not enough to make in a year.

Mae 1:02:13

Oh, no. It's definitely not, but I'm like.

Yannick 1:02:13

But it's were comfortable would start for you.

Lauren 1:02:18

With your basic needs met?

Mae 1:02:20

Yeah.

Lauren 1:02:20

Okay.

Lilly 1:02:28

So personally, I was just taking care of myself, I would say closer to like, 50,000. If it was what I need to do, it would be like 500,000.

Yannick 1:02:43

Because again, it's about that idea of your money is not just your money.

Lilly 1:02:45

Yeah, you can't leave people behind.

.png)

[…]

How much do you believe that one day you will be wealthy as you've just defined it?

Lauren 1:03:03

As I've defined it?

Yannick 1:03:04

As you've defined it. […] Where would you fall?

Lauren 1:03:11

I'll give myself credit.

[…]

Lilly 1:03:21

You ever seen the end of parasite? Yeah, yeah, serious brain trauma going on there.

Yannick 1:03:27

I cannot wait to try and input into my data. The answer to the question was, "Have you seen the end of parasite?"

Lauren 1:03:35

Like when he's living in the basement?

Lilly 1:03:38

It- well no- when the father's in the basement and the son has head trauma and he just thinks that okay, if I just become a millionaire, I can buy the house and get my dad out, right?

Lauren 1:03:47

Oooohh.

Lilly 1:03:48

But he has head trauma, he'll never do it.

[…]

Closing thoughts and discussions

Lauren 1:07:12

(sound of agonized indecision) I feel like I want to ask a question I want to know .... […] I've heard when, like, the gap—when the middle class shrinks so far, and there's such a huge gap in wealth— there's always a revolution, right? So I'm like, what—I'm curious to know something about, like the statistics of like, how long, how far of a gap needs to be there? How long does it need to be there, before people revolt and kill the rich people? Before— How long does it take before the "eat the rich" revolution?

Mae

Sooner than you'd think it'd be.

Lauren

I mean, I feel like history has proven that. and yeah,

Mae

(quiet sing-song) “I'm so hungry.”

Lauren

Is that a clear question?

Yannick

I can chase that. […] That’s clear enough for me to chase.

Lauren

(laughs) Lilly's like, /"fuck you"—

Lilly

/No, it was Mae going, under their breath, "I'm so hungry."

(laughs)

[…]

Mae 1:11:15

[…] (deciding) Question or fact, oh, my God, question or fact?

Yannick 1:11:27

I encourage you not to worry too much about what you ask for, because this project of knowing ourselves is not done, will not be done. And this project is not done, and will continue. So it's not the be all end all. It's just what you would take today.

Lilly 1:11:49

I feel like you could go to a few of these, like have a few of these sessions, because it's so easy to change the answers and react to people's different things and their answers. It's almost a sham—it's like 80 minutes. It's so short.

Yannick 1:12:07

[…] I firmly believe that the ideal length for theater is 45 minutes. My dream is to only make 45 minute things, and I fail every day of my life. But, this is 80 minutes long because I don't responsibly think I can get in and out of this conversation in anything less.

Lilly 1:12:24

It's a lifetime question you'll never have the answer to; you're trying to squeeze in 80 minutes. So you're gonna walk home being like, "Fuck."

Yannick 1:12:31

Well, my hope is that, before you walk home "fuck"ing—

(laughs)

—or as you walk home "fuck"ing, that I didn't give you an answer, but I maybe gave you some questions that you can use to keep walking home. Right? That's, that's the goal. Which is why often—like you could ask a question, or you could for a fact you can say like, "you know, like, I'm not going to solve 'money' today, I'm not gonna solve 'income inequality' today, I just got to get home. I'm not getting home unless you tell me something funny."

(laughs and mmms)

I have something funny, right? If that's what you need. If you're like, "I feel mad, but I could feel madder. And I want to really, like—if we're gonna talk about money, I want to get pissed," I can get your pissed. We can do either, or, at least, the very least I can bring the spice.

Mae

“Can always bring the spice.”

IF WE WIN CBT002-052, September 3rd, 2021

Transcription assistance and Event Photography by Lilly Roman

~

click a session ID to skip ahead, or scroll to read them all

00A-015 | A004-017 | CBT002-052 | back to top

~

IF WE WIN is an ongoing Creative Research Project from Yannick Trapman-O'Brien. Participants receive a lottery ticket in exchange for a providing a breakdown of how they would spend the $25,000 top prize, and together they discuss Money, Wealth, and all the distance in between.

The raw data for participant spending plans and some transcripts can be made available by request to those conducting their own research or creative projects.

Those interested in the exchange above can also check for available slots.